Garagekeepers Coverage Breakdown: Direct Primary, Direct Excess, and Legal Liability

The moment a customer leaves their auto in your care, your automotive business takes on risk, and the type of garage keepers coverage you choose determines how that risk plays out if something goes wrong.

Choosing the right garage keepers option is about more than premium; it’s about customer experience, reputation, and making sure coverage responds the way you expect... when the unexpected happens.

Understanding Garagekeepers Coverage Options

Garage keepers insurance (sometimes called customer auto coverage) is designed to address physical damage to customers’ autos while they are in your care, custody, or control. For automotive businesses, that makes it one of the most important coverages on the policy. It’s also one of the most commonly misunderstood. And to make it more complex, it’s typically available in three different direct coverage options:

- Primary Insurance (Direct Primary)

- Excess Insurance (Direct Excess), and/or

- Legal liability

How Direct Primary Coverage Works: The Customer-First Option

Garage keepers direct primary is the broadest of the options. It generally means your policy can respond before other available coverage for physical damage (e.g., collision, comprehensive/specified cause of loss) to a customer’s auto while it’s in your care, custody, or control. Many shop owners prefer direct primary because it can simplify the conversation with customers and speed resolution.

What owners should consider:

- Risk to reputation and customer reviews when damage isn’t covered. Customers often expect the shop to make things right if you have possession of their automobile.

- How many automobiles you typically have on‑site and the total value — this affects your potential out‑of‑pocket exposure and how often deductibles may apply.

- A common misconception is that direct primary means every situation is covered. In reality, coverage depends on policy terms and how the claim is evaluated.

How Direct Excess Works: Secondary Over the Auto Owner’s Policy

Garage keepers direct excess is often positioned as a middle ground: it normally responds after any collectible insurance from the owner of the automobile, or if the owner doesn’t have physical damage coverage on their policy. This option can help shops extend protection without committing to paying first dollar on every non‑fault loss. Coordination with customers (and their carriers) is key with direct excess.

What owners should consider with direct excess:

- Managing customer expectations when their insurance pays first.

- Extra coordination between carriers can slow down resolution.

- Delays may occur while the customer’s auto coverage is reviewed before yours might apply.

How Legal Liability Works: Fault‑Based Protection

This final option (sometimes referred to as GKLL, which stands for garage keepers legal liability) is designed to respond when the shop is found legally responsible for damage to a customer’s auto. Legal responsibility is determined through the claim investigation and will vary based on the merits of each individual claim.

What owners should consider:

- Thorough intake documentation helps establish what damage was pre‑existing, which is critical when coverage depends on negligence.

- Security and storage procedures matter because coverage may not be afforded if you took reasonable precautions (e.g., hail, theft, vandalism).

- Choosing this option means taking on more reputational risk in exchange for lower premiums, especially for shops whose reputation is white-glove service.

Garagekeepers Insurance Limits, Deductibles, and How to Decide

Regardless of your garage keepers coverage type, most carriers break the limits and deductibles into three key components:

- Per‑location limit: the total limit available for all customer autos at the defined address per occurrence (claim).

- Per‑auto deductibles: the deductible you pay for each auto, per occurrence. If multiple autos are involved, you may be responsible for paying a deductible for each individual auto.

- Event‑level cap (aggregate deductible): The total amount you may pay in deductibles per occurrence (claim). This cap can limit your out-of-pocket expenses, so a single hail or vandalism event doesn’t multiply deductibles indefinitely.

How to determine your limit: A practical rule of thumb is to estimate your peak number of customer autos on‑hand × average value to determine a per-location limit. Then, pressure‑test that number against “bad‑day” scenarios like overnight hail. For auto body and collision repair centers, there are often autos parked outside that need to be taken into consideration. For a lube and oil change facility, the number of bays and automobiles in a bay at any given time is a common way to calculate this limit.

Deductible structures: Per‑automobile deductibles (e.g., $1,000) are common, with some carriers setting a maximum total deductible per event (e.g., $5,000). This per event deductible helps make it so a single loss doesn’t trigger dozens of deductibles. Especially in hail‑prone regions, carriers may not cap the aggregate deductible. Make sure you speak with your insurance provider specifically about the cap to ensure you are well informed on the worst-case scenario with your out-of-pocket expenses.

Annual policy hygiene: Revisit your limits and deductibles at least once a year. Values and the types of autos your shop works on can change (e.g., more EVs, more luxury autos), and expansions or additional storage lots can increase your exposure.

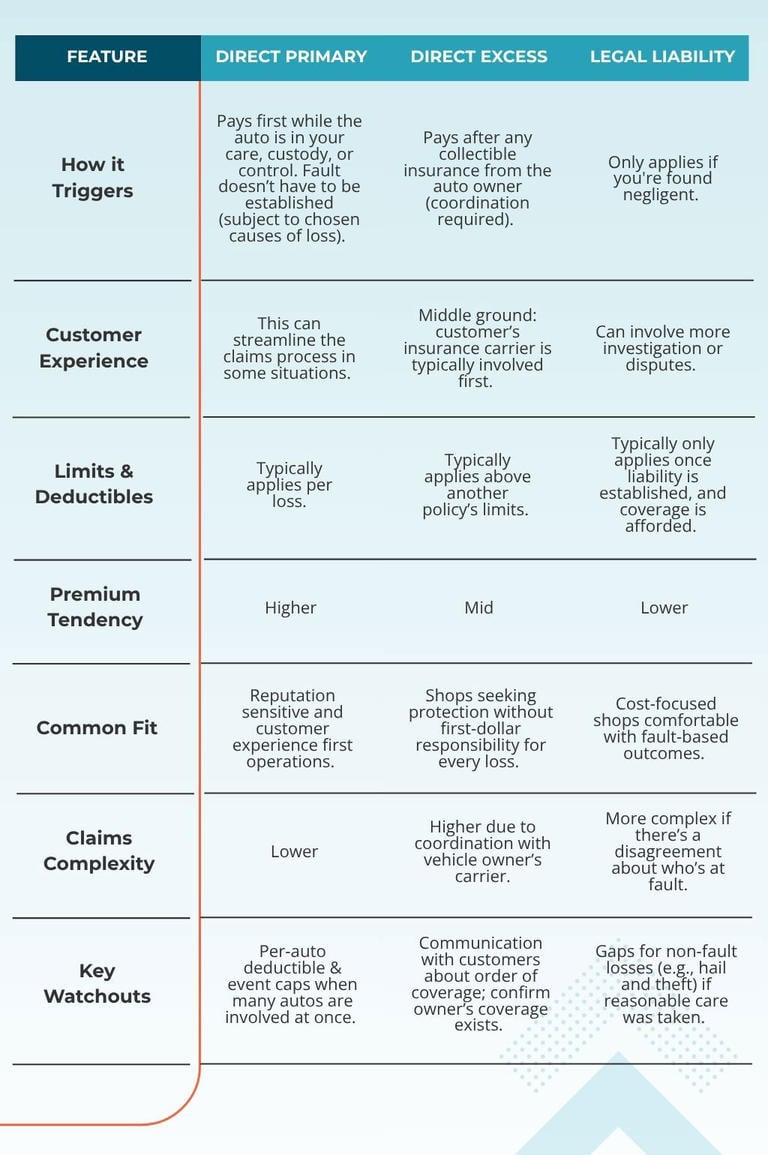

Garagekeepers Coverage Options Comparison Chart: Bringing It All Together

This chart is a simplified comparison for general educational purposes. Actual coverage depends on the policy language and the facts of the individual claim.

What’s Commonly Not Covered Under Garagekeepers Insurance

Though not an exhaustive list, there are common scenarios where coverage is typically excluded under garage keepers insurance, such as:

- Theft or conversion by you, your partners, members, officers, employees, or owners.

- Faulty work or defective parts/materials (the policy does not pay to fix your work).

- Contractual liability (unless you would be liable without the contract).

- Other exclusions shown in your policy (e.g., certain electronics unless permanently installed, racing, war, and pollution).

How Common Garagekeepers Claims May Be Reviewed

These three examples are meant to help explain how garage keepers insurance claims are typically reviewed. Actual outcomes can vary based on the facts of the loss and the terms, conditions, limits, and exclusions of the policy. Coverage is not guaranteed in any of these scenarios.

1: Test Drive Accident: Collision With Another Automobile While Verifying a Repair

Scenario: A technician takes a customer’s auto on a test drive following repairs. During the drive, the auto is involved in an accident that causes damage.

How coverage may apply:

- Direct primary: Coverage may apply to the damage to the customer’s auto, regardless of fault.

- Direct excess: The customer’s auto insurance may respond first. If damages to the customer’s automobile exceed their own policy limits, or the customer doesn’t have physical damage coverage on their policy, the garage keepers direct excess coverage may apply.

- Legal liability: Coverage may apply to the customer’s auto if the shop is found legally responsible for the accident.

Test‑drive accidents often involve more than one part of the policy; when another party is involved in the accident, your garage liability insurance may also factor in. If you want help understanding how these two coverages work together, check out our guide explaining the differences between garage keepers insurance and garage liability insurance.

2: Automobile Theft: Overnight Theft from a Fenced Lot

Scenario: Several customer autos are stolen overnight from the shop’s lot after business hours.

How coverage may apply:

- Direct primary: Coverage may apply to the stolen autos without having to prove negligence (theft by an employee is excluded).

- Direct excess: Individual owners’ auto policies would respond first. The excess coverage may apply only after underlying limits are exhausted, or there is no physical damage coverage on the customer’s auto policy.

- Legal liability: If reasonable care was taken by the shop, coverage may not be afforded under this option.

3: Hailstorm Damage: 10+ Parked Autos Damaged from the Storm

Scenario: A sudden hailstorm damages multiple customer autos stored outside while awaiting new parts for repairs.

How coverage may apply:

- Direct primary: Coverage may apply. Shop owners will likely pay a deductible per auto, up to the per-event cap and the per-location limit. These two limits will determine the full payment.

- Direct excess: The customer’s policies may respond first, with garage keepers coverage potentially applying above those limits. Because these types of scenarios often involve multiple customer autos, many policies are involved, complicating the outcome.

- Legal liability: Coverage may not be afforded if legal responsibility cannot be established.

Hail is one of the most common multi‑auto loss events for shops with outdoor storage. This scenario is where correct per‑location limits and event‑level deductible caps are crucial. With heavy weather, many autos may be hit in one occurrence. It’s critical to confirm how your policy handles perils (like hailstorms) and deductibles for multi-auto events with your insurance provider.

Risk‑Management Solutions to Mitigate Claims

Business insurance is only part of the picture. Proactive risk management can help reduce losses and limit claims frequency. As a business owner, there are a variety of solutions you can put into place to help reduce risk.

Physical Controls

- Install lighting and cameras that record and retain footage. Check camera angles regularly to ensure they actually capture plates and entry points.

- Install fencing or implement controlled access to outdoor lots.

- Bring as many autos inside overnight as space allows.

- Key control: ditch open pegboards. Use locked key boxes or electronic key management with access logs.

Operational Controls

- Establish a thorough intake process with photos/video of each auto (capture all four corners, windshield, interior, etc.). Be sure to also document pre‑existing damage, so you can quickly show what was and wasn’t caused while in your care.

- Develop a ticketing process that follows the autos across bays and lots, and record who last moved a customer’s auto and where it’s parked.

- Create a written test‑drive policy: approved drivers only, defined routes, no personal stops, immediate incident reporting, etc.

- Run Motor Vehicle Records (MVRs) on anyone who may drive customer autos.

Test drive accidents may involve auto damage, third party liability, and employee injury. Shops that tighten driver authorization and MVR standards tend to reduce the frequency and severity of those losses over time.

Weather Readiness

- Develop a “move‑in plan” for high‑value autos when severe weather is on the way.

- Lock down, move, or relocate easily airborne property, where feasible.

Your Owner Checklist to Proactively Protect Your Shop

Pulling it all together, where do you go from here? We’ve put together a checklist to help you get started.

- Review your coverage type, limits, and deductibles each year to ensure they still align with your customer‑experience goals and your tolerance for out‑of‑pocket costs.

- List every location where a customer auto could be stored, even occasionally, on your policy.

- Be aware of outside requirements that may impact your garage keepers insurance: Direct Repair Program (DRPs) requirements, or Franchise Disclosure Documents (FDDs) sometimes specify minimums or response style. Keep copies and share with your insurance partner to ensure your policy is in compliance with requirements.

- Review your policy annually to ensure your limits and exposures account for the current marketplace.

- Has the type of work you do changed?

- Are you working on different kinds of automobiles that are higher or lower in value?

- Has the cost of parts and materials gone up?

- Has your business grown creating more exposure?

- Implement risk control programs as part of your shop’s culture: lighting, key security, MVR checks, etc.

As you evaluate garage keepers insurance, remember it’s only one part of protecting an auto repair business. Our automotive repair business insurance overview provides a complete look at that bigger picture, so you can see how garage keepers insurance fits alongside other essential coverages.

Reviewing Your Garagekeepers Coverage with Confidence

Garage keepers insurance is just one piece of a complete auto service and repair insurance package (workers compensation, garage liability, property, and more). If you want a single partner who understands your business, Intrepid Direct can make it simple and direct.

Because we specialize in the automotive industry, our underwriting, service, and claims teams understand the day‑to‑day realities of repair bays, paint booths, and protecting your customer's automobiles. Talk with one of our industry experts to review your current policy and discuss this critical coverage.

Products and services of Intrepid Direct Insurance described above are provided by one or more insurance company subsidiaries of W. R. Berkley Corporation. Not all products and services may be available in all jurisdictions, and the coverage provided by any insurer is subject to the actual terms and conditions of the policies issued. Information in this publication is subject to change at any time. This publication provides general information only, is not legal advice, and is not a statement of contract. While reasonable care has been utilized in compiling this information, no warranty or representation is made as to accuracy or completeness. Any statement regarding insurance coverage made herein is subject to all provisions and exclusions of the entire insurance policy. Claims scenarios are provided for example purposes only. The outcome of any claim is dependent on the specific facts and circumstances of the claim, as well as the policy provisions in effect at the time of the loss. © 2026 Intrepid Direct Insurance. All rights reserved.

Categories

Recent Posts

Request a Quote

Ready to take control of your insurance? Request a quote and get the coverage you need all in one place. Remember your broker can’t access us and we don’t interfere with their marketing.