Commercial Auto Insurance Options for Franchise Pizza Delivery Operators in 2026

Many delivery-focused franchise restaurant operators have experienced great success over the last 20 years. But today, franchise owners are facing mounting pressure on profitability, driven by rising costs and a more price-sensitive customer.

One cost in particular is increasing faster than most operators expect: commercial auto insurance. And for delivery-focused businesses, it carries significant financial risk.

Inflation continues to challenge profitability for franchisees. Commodity prices for ingredients like cheese and meat remain elevated, while rent, labor, and commercial auto insurance costs have all increased. Competition from third-party delivery platforms and shifting eating habits make it harder to pass along rising costs.

Understanding the Delivery Insurance Challenge: Auto Insurance

Let’s tackle one of these inflationary costs: higher automobile insurance premiums. Pizza operators traditionally have their employees use their personal cars to make deliveries, and drivers are typically reimbursed for expenses. However, that doesn't eliminate the business’s exposure.

If a driver causes an accident while working, the franchisee can still be responsible for damages. If the driver's personal auto insurance limits are not sufficient to cover the damages, or there is no coverage under their personal auto policy, the business may be exposed. The specialty insurance coverage that can step in to protect the business is called Hired and Non-Owned Auto Insurance (HNOA) — it covers your business when employees use their own vehicles to make deliveries.

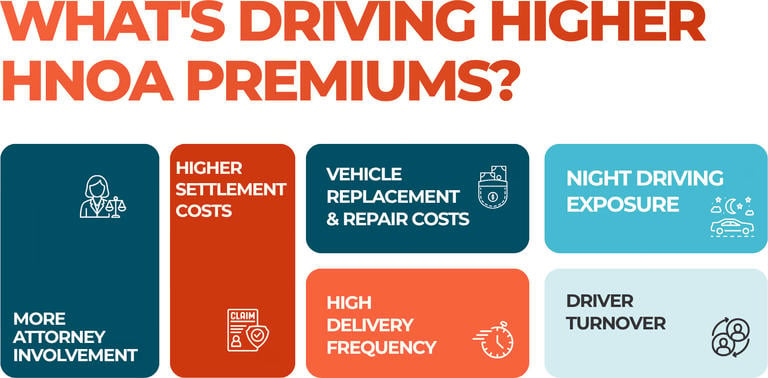

Why Insurance Costs Continue to Rise

The state of the automobile liability insurance market — especially for HNOA — is challenging for insurance companies. You've seen the attorney commercials blanketing every market across the country, and they reflect a broader trend: a more aggressive litigation environment. Accidents today are more likely to involve attorneys, larger demands, and higher settlement costs, putting pressure on insurance premiums. At the same time, vehicle replacement and repair costs have increased significantly, and delivery driving is considered a higher-risk exposure due to night driving, frequent trips, and driver turnover. Together, these factors can make delivery-related injury claims more costly and premiums harder to control.

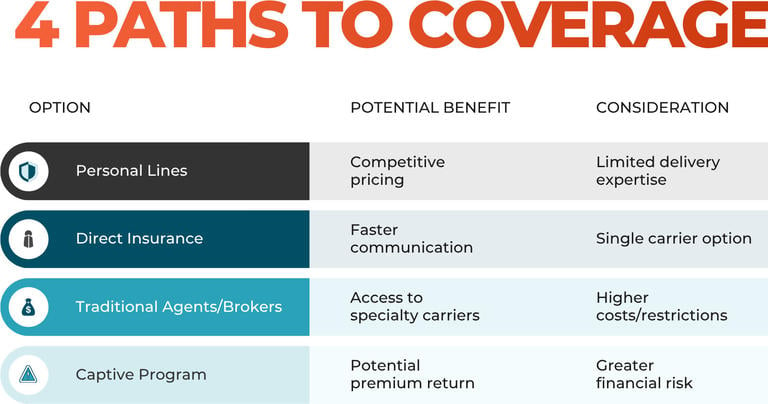

Your Commercial Auto Insurance Options

Traditional Commercial Insurance

Independent agents and brokers offer quotes from the insurance companies with which they're appointed. The challenge? Very few carriers want to write this high-risk insurance coverage right now. As a result, agents and brokers often turn to wholesalers — specialized intermediaries that help them access non-standard insurance carriers for hard-to-place coverage.

What's working: Wholesalers may have access to specialized insurance carriers that aren't available through standard insurance markets, creating options when coverage is difficult to find. They can also help agents and brokers identify new market entrants willing to take on pizza delivery risks. However, even wholesalers have fewer options to choose from than they did in the past.

Considerations: The insurance companies with which wholesalers work often offer higher rates, coverage restrictions, and less flexible payment terms (like payment due in full upfront). These can also be opportunistic markets — an insurance company may enter a market to capitalize on pricing conditions and leave just as quickly if results don't meet expectations, creating less long-term stability for franchise operators.

Traditional Personal Lines Carriers

Insurance carriers that have traditionally focused on personal lines have now entered the pizza delivery market. In many cases, they’re doing so without an established long-term track record in the food delivery segment, often in response to current pricing conditions.

What’s working: These insurance carriers can be very price-competitive and have strong financial ratings.

Considerations: Their depth of expertise in the delivery business can be limited. Personal lines carriers have come and gone in many states and may not have fully understood the severity of pizza delivery risk. In some states, personal lines carriers have pulled back on insuring pizza delivery operators after experiencing higher-than-expected claims activity. Their experience in this specialized space can vary, which over time may impact claims handling and your ability to maintain stable insurance costs.

Direct Insurance

With direct insurance, business owners work directly with the insurance provider, eliminating the need for traditional agents or brokers — and the commissions that come with them.

What's working: Because there are no agent commissions (which can run as high as 25% for HNOA coverage), direct insurance can eliminate one of the larger cost components built into traditional insurance pricing. Direct insurance also creates a more streamlined experience because operators work directly with the insurance provider rather than through multiple intermediaries. Questions can often be addressed more quickly, and decisions related to underwriting, service, and claims are typically made by teams that work together within the same organization.

Considerations: Direct providers only represent themselves, so they can't offer multiple carrier options year after year. Operators looking to compare multiple options will still need to engage independent agents or explore other markets separately. Some independent agents also argue that business owners benefit from having a third-party advocate involved when coverage or claim questions arise.

Captive Insurance Programs

A captive is an insurance entity created for one pizza operator or a group of operators. Captives are typically formed for two reasons: either the operator's loss history is strong enough to justify retaining more risk and profit (versus giving it to an insurance provider), or there aren't enough options available, leading operators to create their own option.

What’s working: A captive creates a new option when other options are limited. If claims are low, franchise pizza operators can receive money back in future years. Captive programs can also enforce stronger risk management requirements, and because the operators are essentially acting as their own insurer, they tend to pay closer attention to safety.

Considerations: Before joining or forming a captive, read the fine print carefully — starting with why it's being created. Agents may be motivated to form captives because they've run out of traditional placement options and have no other way to earn commissions. And if established insurance companies are struggling to make money insuring the pizza delivery space, it's fair to ask why a captive would experience lower claims and generate profits to share with its members.

Captives also face the same market pressures as traditional and direct insurance providers. Reinsurance costs carry the same volatility as the broader market at every renewal, so it's important to understand how much reinsurance is being purchased and who the reinsurers are. While captives can return profits in favorable years, losses are typically borne by the members. These losses may be funded through shared loss funds or additional member assessments, so operators should fully understand how that works before participating. On the claims side, management is typically handled by a third-party administrator (TPA) — and that TPA should be carefully vetted for HNOA-specific experience. It's also worth noting that a pizza franchise risk retention group was placed into liquidation in 2021, leaving operators with unpaid claims and significant financial losses.

Risk Management: The Best Way to Lower Your Premiums

Here's the truth: if pizza delivery operators had zero auto accidents, there'd be a multitude of carriers fighting over the business — which would lower premiums. So how can you lower your chances of an auto accident?

- Strengthen hiring practices. Screen drivers more carefully upfront, including reviewing motor vehicle records (MVRs).

- Reinforce driver training. Invest in real, ongoing driver safety training, not just initial onboarding.

- Invest in technology. Third-party providers like Drivosity and Netradyne can provide tools to monitor driving behavior and improve accountability.

- Build a safety-first culture. Managers need to reinforce safe driving habits as consistently as they focus on operations.

Claims Management: The Part Most Operators Overlook

Claims management is often taken for granted. After an accident happens, how well does your insurance company manage the claim? This matters more than most operators realize.

When evaluating insurance providers, operators should ask themselves:

- Does your carrier have staff with long-term expertise in managing Hired and Non-Owned Auto (HNOA) claims in your state?

- How well do they communicate throughout the claims process?

- How closely do they collaborate with you to achieve fair outcomes?

How claims are managed doesn’t just affect costs in the moment. Just as a credit report reflects financial history, a business's claims history influences future insurance costs and can impact your insurance rates for years. The quality of your claims management today directly impacts the cost of your insurance tomorrow.

Looking Beyond the Next Renewal

The Hired and Non-Owned Auto insurance (HNOA) market will continue to evolve, and operators will likely see new entrants, changing appetites, and shifting pricing over the coming years. While it's tempting to focus solely on finding the lowest premium available today, successful operators should also consider the stability and expertise behind their insurance program. Every delivery creates risk. Every accident can impact your future insurance costs. And every insurance decision affects your profitability.

When comparing HNOA options, ask who will be there when a serious claim occurs, how quickly issues get resolved, and whether the provider has a long-term commitment to the food delivery industry.

Intrepid Direct Insurance has been insuring pizza delivery franchises since 2017 and is a member company of W. R. Berkley Corporation, whose insurance company subsidiaries are rated A+ (Superior) by A.M. Best Company. Because we're direct, our agents, claims professionals, and underwriters all operate under the same roof. Communication is fast because there aren't layers of people between the insurance provider and the franchise pizza operator, and our in-house claims team has built deep expertise in managing delivery-specific claims. Insurance is more than a policy purchase — it's a business relationship that can have a lasting impact on your operation's financial future.

If you're evaluating HNOA coverage, Intrepid Direct can help you compare your options, review your current program, and identify opportunities to better manage your insurance costs. You can also see what our customers are saying on Trustpilot.

Products and services of Intrepid Direct Insurance described above are provided by one or more insurance company subsidiaries of W. R. Berkley Corporation. Not all products and services may be available in all jurisdictions, and the coverage provided by any insurer is subject to the actual terms and conditions of the policies issued. Information in this publication is subject to change at any time. This publication provides general information only, is not legal advice, and is not a statement of contract. While reasonable care has been utilized in compiling this information, no warranty or representation is made as to accuracy or completeness. Any statement regarding insurance coverage made herein is subject to all provisions and exclusions of the entire insurance policy. Claims scenarios are provided for example purposes only. The outcome of any claim is dependent on the specific facts and circumstances of the claim, as well as the policy provisions in effect at the time of the loss. © 2026 Intrepid Direct Insurance. All rights reserved.

Categories

Recent Posts

Request a Quote

Ready to take control of your insurance? Request a quote and get the coverage you need all in one place. Remember your broker can’t access us and we don’t interfere with their marketing.